Despite the fears of an AI Bubble, NVIDIA and their CEO Jensen Huang just announced another stellar quarter of financial results and remain bullish going forward. My friends, let me be blunt: yes, the market took a breath. It seemed like, perhaps, the AI party wouldn’t end in a hangover. But I’ve been around long enough to know that the bigger the party, the harder the fall — and with the scale of commitments being shown by OpenAI, we may be building a tower of chips, data centres and cash flows that’s far more fragile than it looks.

Here’s an insight though: the reason the bubble may burst isn’t a lack of innovation, or even the lack of demand for AI—far from it. The reason is too much concentration of wealth, risk and dependency in too few hands. A single point of failure if you well. And the best illustration of that is this: OpenAI has pledged over $1 trillion in infrastructure and compute deals across data-centers, cloud providers, chip-makers and more.

Pause for a second. A trillion dollars. That’s not a typo. A company with maybe $20 billion in revenue, not even smelling a penny of profit anytime soon, and a pretend valuation of $500 billion is promising to spend more than a trillion dollars in the next decade on wires, racks and GPUs. Where exactly is that money coming from? If OpenAI really becomes the 8,000-pound gorilla in the model/agent wars, maybe it makes sense. But there are plenty of smart people who don’t agree.

Let me walk you through what this means—and why I call it “AI Jenga.”

The Huge Bets

We’ve already seen the headlines:

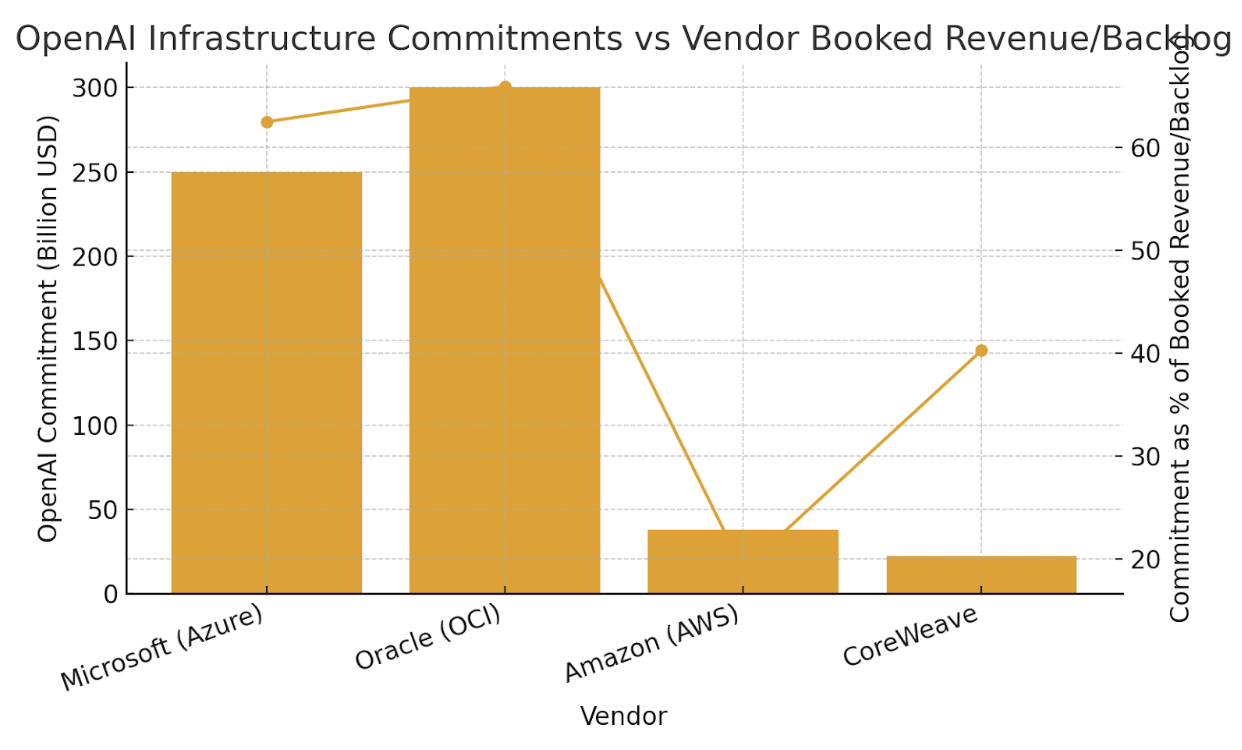

- OpenAI committed north of $300 billion to Oracle Corporation for computing power over the next five years. This is like 66% of Oracle’s revenue forecast.

- It pledged $250 billion with Microsoft for Azure/cloud/data-center plays. A significant portion of Microsoft’s rev projections too.

- With Broadcom, chip-maker partner, deals of hundreds of billions more (in one case the press mentions ~$350 B). This is multiples more than Broadcom’s current revenue.

- Even relatively smaller CoreWeave is in over its head here.

- With AMD and NVIDIA and others, further multi-year hardware deals: e.g., AMD’s 6GW of chips valued at well over $90 B.

These aren’t small bets. They represent significant percentages of the future booked revenues or backlogs for those companies. If OpenAI fails to deliver, or fails to monetize at the scale needed, those companies don’t just lose growth—they face a train-wreck of dependency.

The Jenga Analogy

Imagine a giant Jenga tower. Each block is a piece of compute infrastructure, each set of deals stacked high. OpenAI is pulling a massive block from near the bottom—an “all-in” commitment to spend trillions. If that block comes out and the tower wobbles, all the other blocks (vendors, chip-makers, cloud providers) can come crashing down.

What happens if:

- OpenAI can’t raise sufficient revenue to support the bookings it’s promised. Analysts say its revenue (recently ~ $13 billion) is several orders of magnitude below the scale of its spend.

- One of the vendors—Broadcom, Oracle, Microsoft—finds that their future backlog isn’t sustainable because OpenAI doesn’t fulfill its side.

- A competitor emerges—Anthropic, Google/Alphabet, some surprise “open-source gorilla”—and disrupts the play.

- Markets wake up to the circular financing loops, vendor concentration risks, supply-chain fragility and pull back aggressively.

At that moment, the tower jolts.

Why it Feels Risky to Me

- Concentration of risk: OpenAI becomes the linchpin for dozens of multi-hundred-billion-dollar vendor deals. If it falls, they all fall.

- Vendor dependency: Chip-makers and cloud providers now have huge portions of their future revenues tied to one customer—OpenAI. That’s not diversification; that’s dependency.

- Circular finance: Some of these deals involve vendors funding or investing in OpenAI, while OpenAI buys from them. It’s self-reinforcing—but fragile.

- Revenue mismatch: Even if OpenAI scales massively, it still needs to monetize at absurd speed to justify these commitments.

- Competitor risk: One strategic mis-step, one regulatory glitch, one hardware bottleneck and the advantage may shift away faster than anyone expects.

What This Means For You?

If you’re a DevOps, cybersecurity or AI leader—thinking about cloud strategy, vendor contracts, risk landscapes—here’s my take: don’t assume this tower is stable just because the top blocks shine. Because if the bottom block moves, everything else moves too.

- Treat compute infrastructure as a strategic procurement category, not a commodity.

- Ask: “What happens to my vendor if OpenAI doesn’t deliver what they promised? How exposed are they—and by extension, how exposed is my enterprise?”

- Expect supply–chain shocks. GPU scarcity, data-center buildouts, geopolitical power grids—these aren’t peripheral. They’re core.

- From a cybersecurity lens: a collapse in this infrastructure could ripple out into service disruptions, unexpected vendor exits, or consolidation of power in the hands of fewer vendors.

Sam Altman Gets Credit—Dangerously

Let’s give props where props are due: Sam Altman has pulled off something remarkable. He’s positioned OpenAI as the epicenter of this entire Infra-Planet. If his bet pays off, we’ll call it genius. If it doesn’t… well, we may have just watched the Titanic strike the iceberg.

As more than one analyst noted, the infrastructure commitment (reported at ~$1.4 trillion) is just the starting point. He’s essentially saying: “We’ll build the future ourselves.” But building the future costs money. Lots of money. And money has to come from somewhere.

Shimmy’s Take

In the chase for frontier AI, in the rush to secure hardware, data-centers and cloud muscle, we’re not just playing catch-up with tech. We’re building something epic in scale. But with epic scale comes epic risk.

So yes, AI itself can — and likely will — succeed wildly. But if OpenAI isn’t part of that success equation, if the infrastructure bet fails or lags or misfires… look out below.

This isn’t a warning against AI. It’s a warning about how we’re building AI—with too many hopes riding on too few shoulders, too many bets on one company, and too little margin for error.

My friends, keep your eyes open. Infrastructure matters. Vendor risk matters. Execution matters. Because the bigger the tower we build, the louder the crash when one block gives way.

If the block underneath is OpenAI, and that block cracks—this could be less of a bubble and more of a collapse.