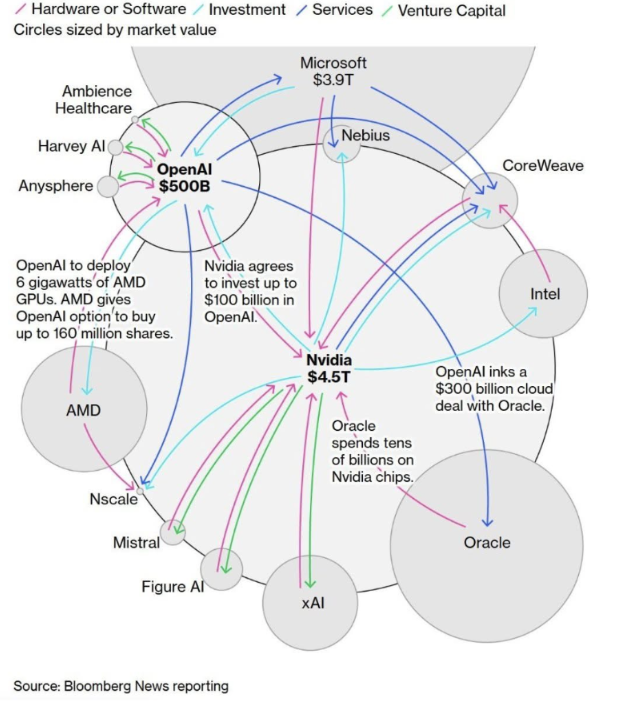

The recent headlines read like an exotic merger of Speed and Infinity: Anthropic striking a multibillion-dollar deal with Google, IBM hooking arms with Groq, and the ever-present NVIDIA, AMD and Oracle executing what looks increasingly like a multi-trillion-dollar tag-team workout. Take a look at the Bloomberg-style diagram attached and you’ll see it — a spaghetti of partnerships, investments, compute-supply deals, and back-and-forth money flows that raise one unavoidable question: Is this real business, or just one big ring-of-friends cheerleading session?

The Bromance in Full Bloom

Let’s start with those two recent moves. Anthropic is in talks with Google for a multibillion-dollar cloud deal — an expansion of their already deep ties. It’s another reminder that compute has become the new currency of power. Meanwhile, IBM and Groq have partnered to accelerate enterprise AI deployment, fusing Groq’s ultra-fast inference technology with IBM’s enterprise credibility.

These moves matter. But when you zoom out to the broader ecosystem, the picture gets fuzzier — and maybe a little unsettling:

- OpenAI is deploying AMD GPUs, with AMD giving OpenAI the option to buy up to 160 million shares.

- NVIDIA agrees to invest up to $100 billion in OpenAI — while OpenAI continues to be one of NVIDIA’s biggest customers.

- Oracle inks a $300 billion cloud deal with OpenAI while simultaneously spending tens of billions on NVIDIA chips.

Look at the diagram long enough and you start seeing loops — company A invests in company B, company B buys product from company A, company C hosts company B’s workloads, and so on. The money, chips, and compute spin around in dizzying orbits.

Now call me skeptical, but when you see this many “friendly” deals — and when the lines between buyer, investor, and supplier blur so completely — you have to ask: Are we witnessing the building of a genuine industrial base for the AI economy, or are we watching a high-stakes circle of insiders trading GPUs and cloud credits in an echo chamber of hype?

Real Commerce — or Vaporware in Disguise?

Let’s be clear: yes, this is a real build-out. The world needs GPUs, cloud capacity, power, and models to drive the AI future. But two things nag at me:

- Revenue circularity: A growing slice of the “AI economy” seems to consist of companies selling to each other — an economic ouroboros. What looks like top-line growth is sometimes just capital spinning around between partners.

- Barrier to entry: These multi-billion-dollar bromances may be great for the insiders, but they risk locking out new innovators who can’t buy their way into the clique. Compute access and capital are quickly becoming gatekeeping mechanisms.

So yes, there’s substance here — but there’s also a structure of self-reinforcement that could come back to bite the industry later.

Winners and Losers in the Great AI Lovefest

Likely Winners:

- NVIDIA and AMD — the chip providers sit at the center of the web. They win no matter who’s training what.

- The hyperscalers — Google, Microsoft, Oracle — their clouds are where the AI lives, breathes, and burns kilowatts.

- Major AI labs — OpenAI, Anthropic, xAI — they have the relationships, the compute, and the brand power.

Potential Losers:

- Startups and independents — anyone without access to cheap GPUs or cloud credits risks being left behind.

- Late entrants — the price of admission is rising fast: chips, data centers, electricity, and talent are scarce and expensive.

- Enterprises who buy into the hype too early — some may find the ROI horizon on these massive AI commitments further out than they were sold.

The “Enemy of My Enemy Is My Friend” Phase

Every tech revolution goes through this “coopetition” stage — when competitors team up because the cost of going it alone is too high. In AI, we’re there now.

Anthropic is deepening ties with Google even as it maintains Amazon and other partnerships. Microsoft backs OpenAI but also invests in Mistral and others. NVIDIA’s money is everywhere. The lines between competition and collaboration are so blurred they’re almost irrelevant. It’s less about who beats whom and more about who can secure the most compute and capital before the next phase of consolidation hits.

But history tells us what comes next: once the land-grab slows, consolidation begins. The “bromance” turns into boardroom battles. And the ones left without scale or differentiation? They get acquired — or disappear.

The Brutal Question: Is This Build-Out Sustainable?

We’re building out data centers and GPU clusters at breakneck speed — faster, perhaps, than demand can justify. Infrastructure costs are skyrocketing; power grids are straining; and regulators are circling. If enterprise adoption and monetization don’t keep pace, this could start to look like the AI version of the dot-com overbuild.

Compute is real, but capital isn’t infinite. The big players can absorb the shock; the smaller ones can’t. The risk isn’t that AI collapses — it’s that it consolidates too quickly into too few hands, and innovation slows to a crawl.

So — What’s My Verdict?

There is real business here. Real chips, real servers, real workloads. But yes — we are absolutely in the bromance phase. Deals are being done at hyperspeed, often as much for optics and leverage as for revenue. The Bloomberg diagram makes that brutally clear — a tangled dance of alliances that feels both strategic and incestuous.

The bromance won’t last forever. But the infrastructure will. And that’s what matters most. When the hype cools, the compute, the data centers, and the tooling will still be there.

If you want to join this dance, don’t just bring a business card — bring power, compute, and something unique to say. Because when the music stops, the folks left holding the GPUs will be just fine. Everyone else? They’ll be wondering whether they were ever part of the band at all.